El Salvador's Bitcoin Volcano

El Salvador's Bitcoin Volcano

Nick Talks Stocks 6/13/2021

Welcome back to Nick Talks Stocks! A weekly newsletter where I cover financial news, stocks, and market trends.

Last issue we talked about the upcoming CPI Data and what it could mean for our economy moving forward. Inflation numbers came in higher than expected, but things are still looking good for an economic recovery through the summer. The Tesla event also passed rather uneventfully, with deliveries for the new Model S beginning on Thursday.

Crypto investors were apart of history this week with El Salvador becoming the first nation to adopt Bitcoin as a legal tender. The decision sparked debate over the efficacy of the El Salvadorian government, but all judgements aside I’m interested to see what happens when Bitcoin is officially adopted into an economy. Following the vote, the country announced a decision to mine bitcoin using volcanic energy, which is certainly the first time I’ve seen that. The outcome is uncertain, but it’s a positive step towards decentralization nonetheless.

Next week’s big catalyst will be the FOMC meeting on June 16th, which will see Chairman Powell take questions alongside a Fed statement. Investors will be eyeing changes to inflation and interest rate forecasts, as interest rates are not expected to change for at least a year. The Fed is also expected to discuss bond tapering, which could act as a negative catalyst to the market. Retail sales and production numbers are scheduled for Tuesday, which will give some insight into the fundamentals of our economy.

Before we start, a few disclaimers. I am not a financial advisor and this is not financial advice. Do your own DD and always know what you own. Got it? Good.

Let's do this.

The markets were green on the week. Growth and tech stocks continue to see strength at the expense of value plays, and the February tech selloff has created some attractive opportunities for fast growing companies. I expect the bullish trend to continue unless the Fed takes some unexpected action towards inflation.

Solar and EVs led the charge as investors turn their focus back towards renewable energy. Demand for such industries is set to explode over the coming years, and governments look to further incentivize electrification through investment and legislation. Enphase Energy (ENPH) is poised to dominate the residential solar market, and they have plans to expand their commercial operations by 2023. The vertical integration of software and diverse hardware solutions gives me confidence in their ability to capture market share going forward. They have a great balance sheet and are growing at an exceptional pace. I’m long Enphase.

The efficient storage of energy is just as important as the method of capturing it. Battery advancements are a critical part of electrification and the transition to renewable energy. Lithium, Nickel, and Cobalt are in high demand due to increased battery production, and those numbers are going to skyrocket in the coming decade. This, along with the growing popularity of EVs, creates an opportunity for producers and miners. The largest American Lithium producer is Albemarle (ABL), but I prefer The Global X Lithium & Battery Tech ETF (LIT) for exposure to the entire industry. With all eyes on the EV industry I wouldn’t be surprised if these stocks catch fire by the end of the year. It’s not the most exciting, but I’m bullish on Lithium.

El Salvador Adopts Bitcoin

On June 8th, 2021 El Salvador became the first nation to adopt Bitcoin as a legal currency:

This is a landmark event for the cryptocurrency community and hopefully it serves to give Bitcoin some legitimacy on the world stage. Now that El Salvador has sparked the movement, I wouldn’t be surprised to see some small nations follow suit, especially those who have adopted the U.S. Dollar.

The effects of this are impossible to predict. My main concern is the volatility, as currencies are supposed to be stable and Bitcoin is anything but. Wild swings in purchasing power are going to make it difficult to forecast monetary conditions and I can see that effecting consumers. At the same time Bitcoin brings people monetary freedom, which is a good cause. I have no idea how this goes, I’m just interested to see what happens.

Oh yeah, and they’re mining Bitcoin with volcanoes. Only in El Salvador.

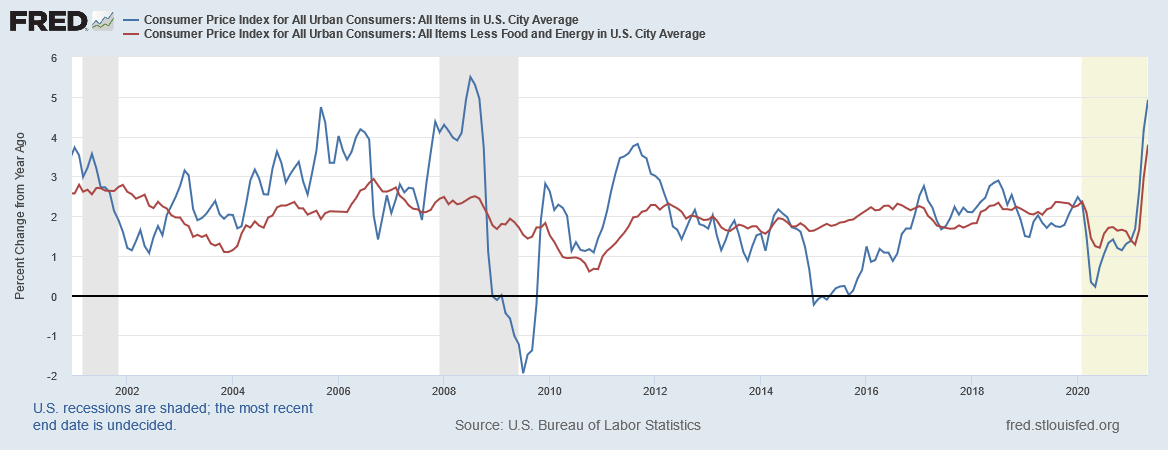

CPI Data

May’s CPI numbers were released Thursday giving insight into the current inflation situation. The Index gained 0.6% relative to April, which exceeded expectations of 0.4%. While high, I remain unconcerned as numbers appear to be slowing down. As long as the current trend continues, inflation should prove to be transitory. The year over year growth of 5% appears bad, but consider the low point of comparison during COVID. Ignoring the COVID shock, long term inflation is on the same pace as the end of 2019.

The high CPI numbers were driven mainly by gas and used car sales. Oil is coming off of lows in 2020, and that, combined with a Democratic administration and inflationary environment, creates the perfect case for gas prices to soar. Used car prices are up 20% this year due to semiconductor shortages, which leads to less production of new cars. People still need to buy cars, so they resort to used vehicles, driving up the price.

Inflation is certainly something to keep on eye on, but we’re far from being out of control. I still believe we’re facing long term deflationary pressures as technology becomes more efficient and production cheaper. The only concerns I have regarding inflation are subsequent changes to bond purchases and interest rates, which should be discussed at the upcoming FOMC meeting.

Looking Ahead

The June FOMC meeting is on Wednesday, which will give clarity on bond purchases, as well as revisions to the Fed’s monetary forecast. These meetings often serve as market movers, and I’m expecting multiple catalysts in the week ahead. I wouldn’t be surprised to see inflation projections increase following the recent data, as the Fed should err on the side of caution with regards to overheating the economy. Additionally, the Fed will likely discuss tapering bond purchases, which I expect to actually occur sometime in the Fall.

The Fed must precariously balance inflation concerns with asset prices. Raise rates too soon and we may see a sharp drop in real estate and equity values, but take too long and we may get runaway inflation. They will eventually have to be raised, as keeping rates near zero is not sustainable in the long term. We may never see interest rates go back above 5% however, as global economies enter a new paradigm of low rates.

Investors are looking for clarity before jumping into the market. A selloff is possible depending on how the meeting goes, especially if they mention tapering bond purchases before the end of this year. A revision to inflation numbers would also likely move the markets, impacting growth stocks the most. The meeting could also cause markets to rally, as investors get the clarity they need to make purchases. Either way, the effects shouldn’t be hugely significant unless something unexpected happens.

See you all next week,